| Citation: |

Zhaowei Tian, Shuying Zhai, Zhifeng Weng. COMPACT FINITE DIFFERENCE SCHEMES OF THE TIME FRACTIONAL BLACK-SCHOLES MODEL[J]. Journal of Applied Analysis & Computation, 2020, 10(3): 904-919. doi: 10.11948/20190148

|

COMPACT FINITE DIFFERENCE SCHEMES OF THE TIME FRACTIONAL BLACK-SCHOLES MODEL

-

Abstract

In this paper, three compact difference schemes for the time-fractio-nal Black-Scholes model governing European option pricing are presented. Firstly, in order to obtain the fourth-order accuracy in space by applying the Padé approximation, we eliminate the convection term of the B-S equation by an exponential transformation. Then the time fractional derivative is approximated by $ L1 $ formula, $ L2 - 1_\sigma $ formula and $ L1 - 2 $ formula respectively, and three compact difference schemes with oders $ O(\Delta t^{2-\alpha}+h ^4) $, $ O(\Delta t^{2}+h ^4) $ and $ O(\Delta t^{3-\alpha}+h ^4) $ are constructed. Finally, numerical example is carried out to verify the accuracy and effectiveness of proposed methods, and the comparisons of various schemes are given. The paper also provides numerical studies including the effect of fractional orders and the effect of different parameters on option price in time-fractional B-S model. -

-

References

[1] A. A. Alikhanov, A new difference scheme for the time fractional diffusion equation, J. Comput. Phys., 2015, 280, 424-438. doi: 10.1016/j.jcp.2014.09.031 [2] F. Black, M. Scholes, The pricing of options and corporate liabilities, J. Polit. Econ., 1973, 81(3), 637-654. doi: 10.1086/260062 [3] P. Carr, L. Wu, The finite moment log stable process and option pricing, J. Finance, 2003, 58(2), 597-626. [4] A. Cartea, D. del-Castillo-Negrete, Fractional diffusion models of option prices in markets with jumps, Phys. A: Stat. Mech. Appl., 2007, 374(2), 749-763. [5] W. T. Chen, X. Xu, S. P. Zhu, Analytically pricing European-style options under the modified Black-Scholes equation with a spatial-fractional derivative, Q. Appl. Math., 2014, 72(3), 597-611. doi: 10.1090/S0033-569X-2014-01373-2 [6] A. Cartea, Derivatives pricing with market point processes using tick-by-tick data, Q. Finance, 2013, 13(1), 111-123. [7] W. T. Chen, X. Xu, S. P. Zhu, Analytically pricing double barrier options based on a time-fractional Black-Scholes equation, Comput. Math. Appl., 2015, 69(12), 1407-1419. doi: 10.1016/j.camwa.2015.03.025 [8] W. T. Chen, B. W. Yan, G. H. Lian et al., Numerically pricing American options under the generalized mixed fractional Brownian motion model, Phys. A: Stat. Mech. Appl., 2016, 451, 180-189. doi: 10.1016/j.physa.2015.12.154 [9] Z. D. Cen, J. Huang, A. M. Xu et al., Numerical approximation of a time-fractional Black-Scholes equation, Comput. Math. Appl., 2018, 8(75), 2874-2887. [10] G. H. Gao, Z. Z. Sun, H. W. Zhang, A new fractional numerical differentiation formula to approximate the Caputo fractional derivative and its applications, J. Comput. Phys., 2014, 259, 33-50. doi: 10.1016/j.jcp.2013.11.017 [11] G. Jumarie, Derivation and solutions of some fractional Black-Scholes equations in coarse-grained space and time. Application to Merton's optimal portfolio, Comput. Math. Appl., 2010, 59(3), 1142-1164. doi: 10.1016/j.camwa.2009.05.015 [12] M. N. Koleva, L. G. Vulkov, Numerical solution of time-fractional Black-Scholes equation, J. Comput. Appl. Math., 2017, 36 (4), 1699-1715. [13] J. R. Liang, J. Wang, W. J Zhang et al., The solutions to a bi-fractional Black-Scholes-Merton differential equation, Int. J. Pure Appl. Math., 2010, 58(1), 99-112. [14] W. Y. Liao, A compact high-order finite difference method for unsteady convection-diffusion equation, Int. J. Comput. Meth. Eng. Sci. Mech., 2012, 13(3), 135-145. [15] B. Mandelbrot, The variation of certain speculative prices, J. Bus. Univ. Chicago, 1963, 36, 394-419. [16] L. N. Song, W. G. Wang, Solution of the fractional Black-Scholes option pricing model by finite difference method, Abstr. Appl. Anal., 2013, Article ID 194286, 1-10. [17] R. H. De Staelen, A. S. Hendy, Numerically pricing double barrier options in a time-fractional Black-Scholes model, Comput. Math. Appl., 2017, 74, 1166-1175. doi: 10.1016/j.camwa.2017.06.005 [18] Z. Z. Sun, G. H. Gao, Finite Difference Methods for Fractional Differential Equations, Science Press, Beijing, 2015. [19] W. Wyss, The fractional Black-Scholes equations, Fract. Calc. Appl. Anal., 2000, 3(1), 51-61. [20] X. Z. Yong, X. Zhang, L. F. Wu, A kind of efficient difference method for time-fractional option pricing model, Appl. Math. J. Chin. Univ., 2015, 30(2), 234-244. [21] X. Z. Yang, L. F. Wu, S. Z. Sun et al., A universal difference method for time-space fractional Black-Scholes equation, Adv. Differ. Equ., 2016, 71, 1-14. [22] H. M. Zhang, F. W. Liu, I. Turner et al., The numerical simulation of the tempered fractional Black-Scholes equation for European double barrier option, Appl. Math. Model., 2016, 40(11-12), 5819-5834. doi: 10.1016/j.apm.2016.01.027 [23] H. M. Zhang, F. W. Liu, I. Turner et al., Numerical solution of the time fractional Black-Scholes model governing European options, Comput. Math. Appl., 2016, 71(9), 1772-1783. doi: 10.1016/j.camwa.2016.02.007 [24] Y. Zhang, X. Z. Yang, Pure alternative segment explicit-implicit parallel difference methods for time-fractional Black-Scholes equation, China Science Paper, 2017, 12(17), 1966-1971. [25] Z. Q. Zhou, X. M. Gao, Numerical methods for pricing American options with time-fractional PDE models, Math. Prob. Eng., 2016, Article ID 5614950, 1-8. -

-

Figures(3) / Tables(4)

Export File

Citation

Zhaowei Tian, Shuying Zhai, Zhifeng Weng. COMPACT FINITE DIFFERENCE SCHEMES OF THE TIME FRACTIONAL BLACK-SCHOLES MODEL[J]. Journal of Applied Analysis & Computation, 2020, 10(3): 904-919. doi: 10.11948/20190148

Format

Content

DownLoad:

DownLoad:

-

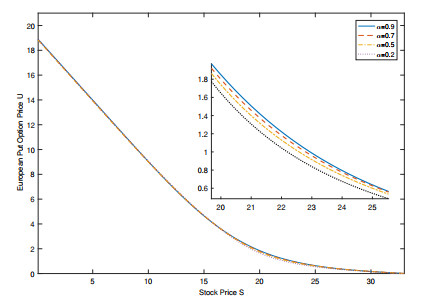

Figure 1. Curves of European put option with different

$ \alpha $ . -

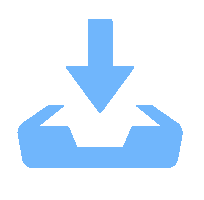

Figure 2. Curves of European call option with different

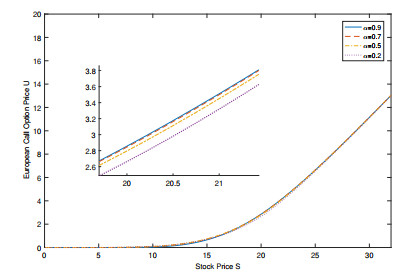

$ \alpha $ - Figure 3. Curves of European put option with different values of parameters