| Citation: |

Xiaofeng Yan, Haiyan Wang, Yulian An. FORECASTING SYSTEMIC RISK OF CHINA'S BANKING INDUSTRY BY PARTIAL DIFFERENTIAL EQUATIONS MODEL AND COMPLEX NETWORK[J]. Journal of Applied Analysis & Computation, 2023, 13(6): 3632-3654. doi: 10.11948/20230306

|

FORECASTING SYSTEMIC RISK OF CHINA'S BANKING INDUSTRY BY PARTIAL DIFFERENTIAL EQUATIONS MODEL AND COMPLEX NETWORK

-

Abstract

The monitoring and controlling of systemic risk have increasingly become the focus of attention in the financial field. It is important and difficult to accurately forecast systemic financial risk. In this paper, we propose a spatio-temporal partial differential equation model to describe the systemic risk of China's Banking Industry based on network, clustering, and real date of 24 China's A-share listed banks. The model considers the combined influence of local risk and transboundary contagion effects, and the prediction relative accuracy is up to 95%. Simulation results confirm that strict joint control measures, the timeliness of central bank intervention, and differences in bank strategies are efficient for reducing systemic risk. To our knowledge, this is the first paper to apply a PDE model to forecast systemic financial risk.

-

Keywords:

- Systemic risk /

- forecast /

- complex network /

- partial differential equation /

- joint control

-

-

References

[1] D. Acemoglu, A. Ozdaglar and A. Tahbaz-Salehi, Systemic risk and stability in financial networks, National Bureau of Economic Research, Inc, 2013, (2). DOI: 10.1257/aer.20130456. [2] V. V. Acharya, L. H. Pedersen, T. Philippon and M. Richardson, Measuring systemic risk, The review of financial studies, 2017, 30(1), 2-47. DOI: 10.1093/rfs/hhw088. [3] T. Adrian and M. K. Brunnermeier, CoVaR, Tech. rep., National Bureau of Economic Research, 2011. DOI: http://www.nber.org/papers/w17454 .[4] M. Alexandre, T. C. Silva, C. Connaughton and F. A. Rodrigues, The drivers of systemic risk in financial networks: a data-driven machine learning analysis, Chaos, Solitons & Fractals, 2021, 153, 111588. DOI: 10.1016/j.chaos.2021.111588. [5] F. Allen and D. Gale, Financial contagion, Journal of political economy, 2000, 108(1), 1-33. DOI: 10.1086/262109. [6] L. Allen, T. G. Bali and Y. Tang, Does systemic risk in the financial sector predict future economic downturns?, The Review of Financial Studies, 2012, 25(10), 3000-3036. DOI: 10.1093/rfs/hhs094. [7] S. Behrendt, T. Dimpfl, F. J. Peter and D. J. Zimmermann, Rtransferentropy—quantifying information flow between different time series using effective transfer entropy, SoftwareX, 2019, 10, 100265. DOI: 10.1016/j.softx.2019.100265. [8] A. R. Benson, D. F. Gleich and J. Leskovec, Higher-order organization of complex networks, Science, 2016, 353(6295), 163-166. DOI: 10.1126/science.aad9029. [9] M. Billio, M. Getmansky, A. W. Lo and L. Pelizzon, Econometric measures of connectedness and systemic risk in the finance and insurance sectors, Journal of financial economics, 2012, 104(3), 535-559. DOI: 10.1016/j.jfineco.2011.12.010. [10] R. Bookstaber, M. Paddrik and B. Tivnan, An agent-based model for financial vulnerability, Journal of Economic Interaction and Coordination, 2018, 13(2), 433-466. DOI: 10.1016/j.jbankfin.2013.02.032. [11] F. Brauer, Compartmental models in epidemiology, Mathematical epidemiology, 2008, 19-79. DOI: 10.1007/978-3-540-78911-6. [12] C. Brownlees and R. F. Engle, Srisk: A conditional capital shortfall measure of systemic risk, The Review of Financial Studies, 2017, 30(1), 48-79. DOI: 10.1093/rfs/hhw060. [13] L. Faes, D. Marinazzo, A. Montalto and G. Nollo, Lag-specific transfer entropy as a tool to assess cardiovascular and cardiorespiratory information transfer, IEEE Transactions on Biomedical Engineering, 2014, 61(10), 2556-2568. DOI: 10.1109/TBME.2014.2323131. [14] D. Fanelli and F. Piazza, Analysis and forecast of COVID-19 spreading in china, italy and france, Chaos, Solitons & Fractals, 2020, 134, 109761. DOI: 10.1016/j.chaos.2020.109761. [15] A. Friedman, Partial Differential Equations of Parabolic Type, Courier Dover Publications, 2008. DOI: 10.1007/978-3-0348-7922-4. [16] Y.-C. Gao, R. Tan, C.-J. Fu and S.-M. Cai, Revealing stock market risk from information flow based on transfer entropy: The case of chinese a-shares, Physica A: Statistical Mechanics and its Applications, 2023, 128982. DOI: 10.1016/j.physa.2023.128982. [17] C.-P. Georg, The effect of the interbank network structure on contagion and common shocks, Journal of Banking & Finance, 2013, 37(7), 2216-2228. DOI: 10.1016/j.jbankfin.2013.02.032. [18] R. Greenwood, A. Landier and D. Thesmar, Vulnerable banks, Journal of Financial Economics, 2015, 115(3), 471-485. DOI: 10.1016/j.jfineco.2014.11.006. [19] K. Hlavácková-Schindler, Equivalence of granger causality and transfer entropy: A generalization, Applied Mathematical Sciences, 2011, 5(73), 3637-3648. DOI: https://www.researchgate.net/publication/233965869. [20] Z. Jing, Z. Liu, L. Qi and X. Zhang, Spillover effects of banking systemic risk on firms in china: A financial cycle analysis, International Review of Financial Analysis, 2022, 82, 102171. doi: 10.1016/j.irfa.2022.102171 [21] A. Karlekar, A. Seal, O. Krejcar and C. Gonzalo-Martin, Fuzzy k-means using non-linear s-distance, IEEE Access, 2019, 7, 55121-55131. DOI: 10.1109/ACCESS.2019.2910195. [22] G. G. Kaufman and K. E. Scott, What is systemic risk, and do bank regulators retard or contribute to it?, The independent review, 2003, 7(3), 371-391. DOI: http://www.jstor.org/stable/24562449. [23] Y. Kim, J. Kim and S.-H. Yook, Information transfer network of global market indices, Physica A: Statistical Mechanics and its Applications, 2015, 430, 39-45. DOI: 10.1016/j.physa.2015.02.081. [24] J. C. Lagarias, J. A. Reeds, M. H. Wright and P. E. Wright, Convergence properties of the nelder-mead simplex method in low dimensions, SIAM Journal on optimization, 1998, 9(1), 112-147. DOI: 10.1137/S1052623496303470. [25] J. D. Murray, Mathematical Biology: I. An Introduction, Springer, 2002. DOI: https://doi.org/10.1007/978-0-387-22437-4 .[26] J. D. Murray, Reaction diffusion, chemotaxis, and nonlocal mechanisms, Mathematical Biology: I. An Introduction, 2002, 395-417. DOI: 10.1007/978-0-387-22437-4. [27] M. S. Murugan, et al., Large-scale data-driven financial risk management & analysis using machine learning strategies, Measurement: Sensors, 2023, 27, 100756. DOI: 10.1016/j.measen.2023.100756. [28] I. V. Oseledets, Tensor-train decomposition, SIAM Journal on Scientific Computing, 2011, 33(5), 2295-2317. DOI: 10.1137/090752286. [29] L. Riccetti, Systemic risk analysis and sifis detection: A proposal for a complete methodology, Available at SSRN 3415730, 2019. DOI: 10.2139/ssrn.3415730 .[30] M. S. Risk and R. F. Soundness, Global financial stability report, International Monetary Fund, Washington, 2008. [31] T. Schreiber, Measuring information transfer, Physical review letters, 2000, 85(2), 461. DOI: 10.1103/PhysRevLett.85.461. [32] F. Sekmen and M. Kurkcu, An early warning system for turkey: the forecasting of economic crisis by using the artificial neural networks, Asian Economic and Financial Review, 2014, 4(4), 529-543. DOI: https://archive.aessweb.com/index.php/5002/article/view/1176. [33] K. K. Sharma and A. Seal, Spectral embedded generalized mean based k-nearest neighbors clustering with s-distance, Expert Systems with Applications, 2021, 169, 114326. DOI: 10.1016/j.eswa.2020.114326. [34] J. Shi, C. Wang, H. Wang and X. Yan, Diffusive spatial movement with memory, Journal of Dynamics and Differential Equations, 2020, 32, 979-1002. DOI: 10.1007/s10884-019-09757-y. [35] T. C. Silva, M. A. da Silva and B. M. Tabak, Systemic risk in financial systems: a feedback approach, Journal of Economic Behavior & Organization, 2017, 144, 97-120. DOI: 10.1016/j.jebo.2017.09.013. [36] H. Smaoui, K. Mimouni, H. Miniaoui and A. Temimi, Funding liquidity risk and banks' risk-taking: Evidence from islamic and conventional banks, Pacific-Basin Finance Journal, 2020, 64, 101436. doi: 10.1016/j.pacfin.2020.101436 [37] P. Song and Y. Xiao, Estimating time-varying reproduction number by deep learning techniques, J. Appl. Anal. Comput., 2022, 12(3), 1077-1089. DOI: 10.11948/20220136. [38] J. Suss and H. Treitel, Predicting Bank Distress in the UK with Machine Learning, 2019. DOI: 10.2139/ssrn.3465753 .[39] A. Tobias and M. K. Brunnermeier, Covar, The American Economic Review, 2016, 106(7), 1705-1741. DOI: 10.1257/aer.20120555. [40] E. Tölö, Predicting systemic financial crises with recurrent neural networks, Journal of Financial Stability, 2020, 49, 100746. DOI: 10.1016/j.jfs.2020.100746. [41] G.-J. Wang and C.-L. Zhu, BP-CVAR: A novel model of estimating cvar with back propagation algorithm, Economics Letters, 2021, 209, 110-125. DOI: 10.1016/j.econlet.2021.110125. [42] H. Wang, F. Wang and K. Xu, Modeling information diffusion in online social networks with partial differential equations, 7, 2020. DOI: 10.48550/arXiv.1310.0505 .[43] L. Wang, S. Li and T. Chen, Investor behavior, information disclosure strategy and counterparty credit risk contagion, Chaos, Solitons & Fractals, 2019, 119, 37-49. DOI: 10.1016/j.chaos.2018.12.007. [44] Y. Wang and H. Wang, Using networks and partial differential equations to forecast bitcoin price movement, Chaos: An Interdisciplinary Journal of Nonlinear Science, 2020, 30(7), 073127. DOI: 10.1063/5.0002759. [45] Y. Wang, H. Wang, S. Chang and A. Avram, Prediction of daily pm 2.5 concentration in china using partial differential equations, PloS one, 2018, 13(6), e0197666. DOI: 10.1371/journal.pone.0197666. [46] Y. Wang, H. Wang and S. Zhang, Quantifying prediction and intervention measures for PM2.5 by a PDE model, Journal of Cleaner Production, 2020, 268, 122-131. DOI: 10.1016/j.jclepro.2020.122131. [47] L. Yang, T. Gao, Y. Lu, et al., Neural network stochastic differential equation models with applications to financial data forecasting, Applied Mathematical Modelling, 2023, 115, 279-299. DOI: 10.1016/j.apm.2022.11.001. [48] W. Zhang, X. Zhuang, J. Wang and Y. Lu, Connectedness and systemic risk spillovers analysis of chinese sectors based on tail risk network, The North American Journal of Economics and Finance, 2020, 54, 101248. DOI: 10.1016/j.najef.2020.101248. -

-

Figures(14) / Tables(5)

Export File

Citation

Xiaofeng Yan, Haiyan Wang, Yulian An. FORECASTING SYSTEMIC RISK OF CHINA'S BANKING INDUSTRY BY PARTIAL DIFFERENTIAL EQUATIONS MODEL AND COMPLEX NETWORK[J]. Journal of Applied Analysis & Computation, 2023, 13(6): 3632-3654. doi: 10.11948/20230306

Format

Content

DownLoad:

DownLoad:

-

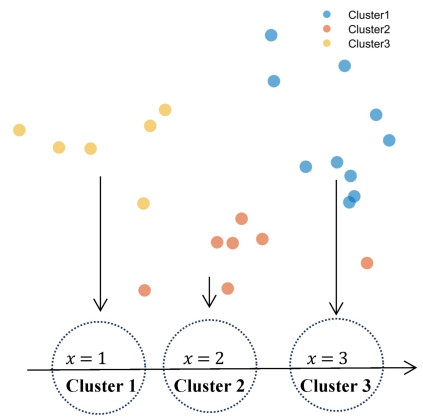

Figure 1.

Three clusters embedded in one-dimensional space

-

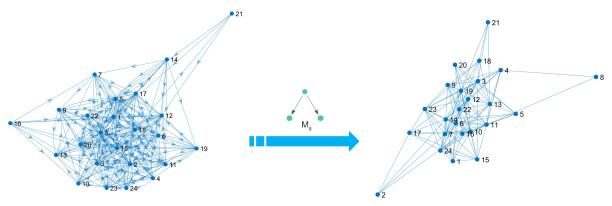

Figure 2.

The directed graph

$ \tilde{G} $ $ G $ -

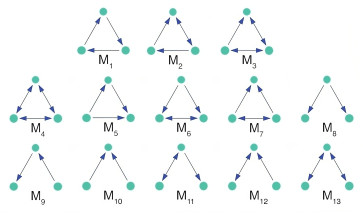

Figure 3.

Triangle motifs

-

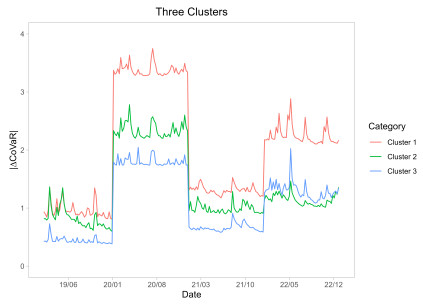

Figure 4.

The weighted average of

$ |\Delta \mbox{CoVaR}| $ $ |\Delta\mbox{CoVaR}| $ $ |\Delta \mbox{CoVaR}| $ -

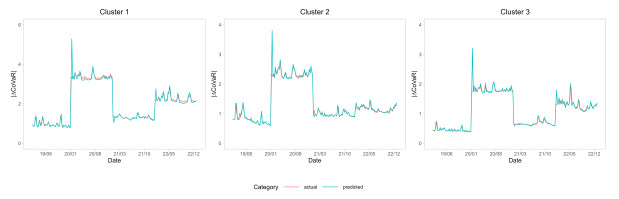

Figure 5.

The weighted average of

$ |\Delta\mbox{CoVaR}| $ $ |\Delta\mbox{CoVaR}| $ $ |\Delta\mbox{CoVaR}| $ -

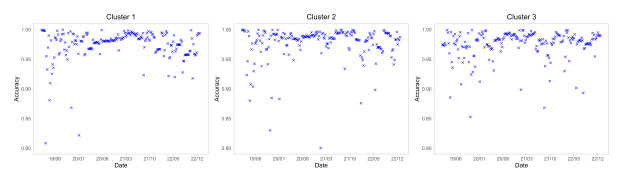

Figure 6.

The relative accuracy (RA) in Cluster 1, Cluster 2 and Cluster 3 from 2019 to 2022.

-

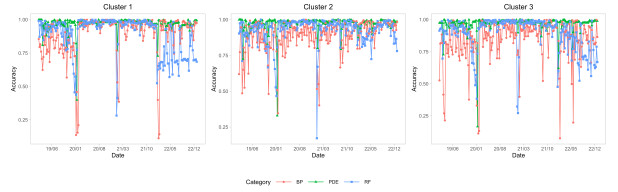

Figure 7.

Comparison of the relative accuracy (RA) among PDE model, BP neural network model and Random Forest model

-

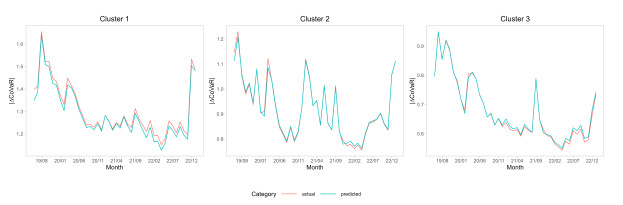

Figure 8.

Month-Forecast of weighted

$ |\Delta\mbox{CoVaR}| $ -

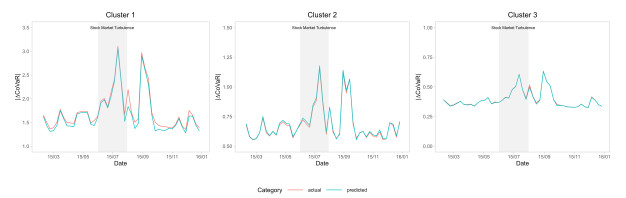

Figure 9.

Week-Forecast of weighted

$ |\Delta\mbox{CoVaR}| $ -

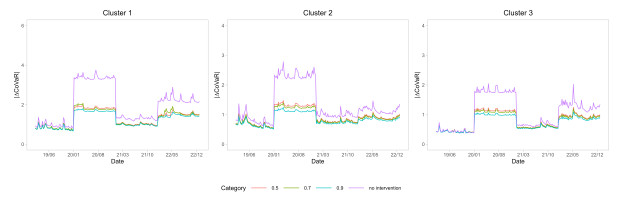

Figure 10.

The weighted

$ |\Delta\mbox{CoVaR}| $ -

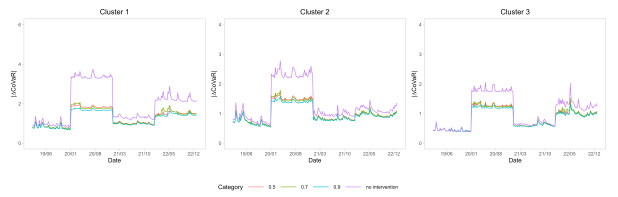

Figure 11.

The weighted

$ |\Delta\mbox{CoVaR}| $ -

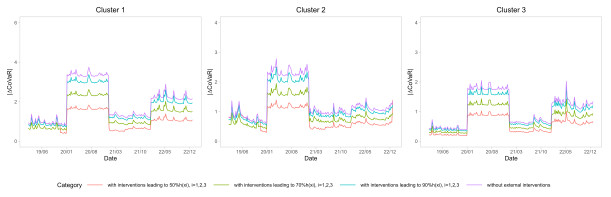

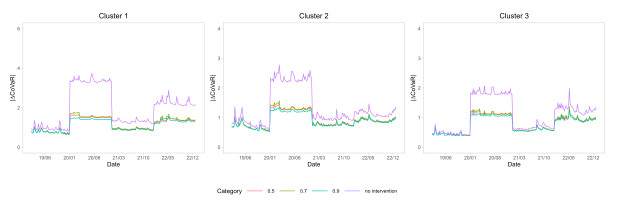

Figure 12.

The

$ |\Delta\mbox{CoVaR}| $ $ \xi=0.3, \phi=0.4 $ -

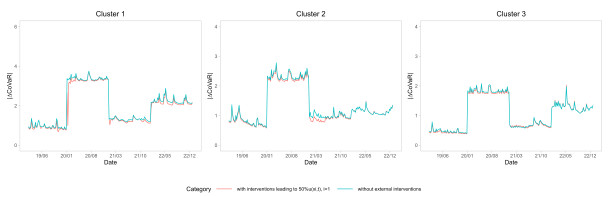

Figure 13.

The

$ |\Delta\mbox{CoVaR}| $ $ \kappa=0.3, \phi=0.4 $ -

Figure 14.

The

$ |\Delta\mbox{CoVaR}| $ $ \kappa=0.3, \xi=0.3 $